It is too early to make any definitive statements on how the Trump administration will affect global markets and economies, but a few key themes stand out:

1) Tariff targets

The first is that Trump has made clear he intends to raise tariffs on imported goods, with China likely facing the brunt of the increases.

2) Cuts

The second is that he plans to cut US taxes and regulations, though it is not yet clear how deep the cuts will be and how the tax cuts will be paid for.

3) America First

And third, on the geopolitical front, his early administration appointments indicate he will likely pursue an “America First” isolationist-leaning, transactional foreign policy, similar to his first term.

Market reaction

The initial market reaction to his win has been relatively orderly, with US risk assets and the US dollar out-performing, and government bond yields stabilising following a large pre-election rise. Looking forward, a key risk to the outlook is a potential back-up in US government bond yields (with ripple effects through global markets) if the new Trump administration tries to push through tax cuts without a credible plan to pay for them.

Trade war?

Another key risk is an escalatory tit-for-tat global trade war that disrupts supply chains and drives global growth lower and (initially) drives inflation higher. Our base case is that cooler minds will prevail, and worst-case scenarios will be avoided, allowing the current global economic expansion to extend through 2025. However, Trump is notoriously unpredictable and without the constraints of divided government, his policies and the global outlook have the potential to change quickly.

Investors should prepare for higher for longer US rates, higher public market volatility, and focus on companies’ supply chain resilience and potential direct and indirect exposures to US tariffs

Manageable impact on Europe

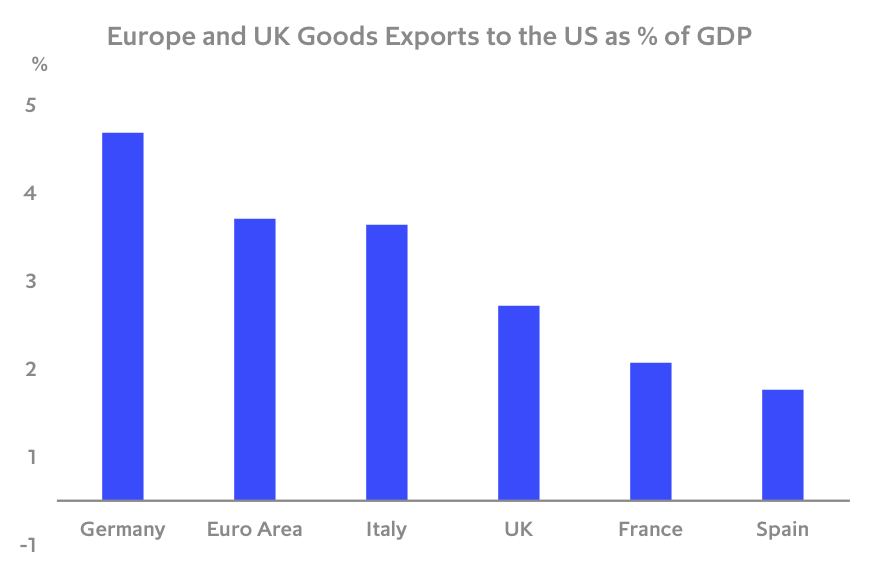

In terms of the potential direct growth impact on Europe, to put things in perspective, Europe’s goods exports to the US in 2023 were equivalent to around 3.2% of GDP. Even for Germany, the most exposed of Europe’s economies, goods exports to the US were equivalent to 4.2% of GDP. UK goods exports to the US are equivalent to 2.2% of GDP. The manufacturing sector makes up around 15% and the services sector makes up over 80% of Europe’s GDP. While services companies servicing domestic goods exporters exposed to the US may be affected, most services sector companies should see little direct impact from higher US goods tariffs.

Europe and UK goods exports to the US as % of GDP

Therefore, if Trump follows through on his threat to raise import tariffs on goods, while they will have potentially large consequences for parts of Europe’s manufacturing sector – autos, pharmaceuticals and machinery in particular – and may have secondary effects on companies servicing them, the impact on the broader Europe and UK economies should be manageable in our view. The inflation impact is expected to be negligible given already weak underlying inflation pressures and likely only token highly targeted retaliatory tariffs.

Read full report

What does Trump’s election win mean for the global economy? is available in full on the ICG website.